RBI Cybersecurity Requirements: A Beginner's Guide (2026)

RBI cybersecurity requirements explained for beginners — Master Direction, Baseline Cyber Security Controls, CERT-In rules, who is regulated, costs, and a step-by-step compliance roadmap for 2026.

If you run technology, security, or compliance for a bank, NBFC, payment aggregator, prepaid instrument issuer, or fintech in India, the Reserve Bank of India (RBI) has expectations of you that grow more specific every year. This is the plain-language map most regulated entities wish they had on day one — what RBI actually demands, who it applies to, what auditors actually check for, and how to plan a credible 12-month compliance journey from scratch.

RBI does not publish a single "cybersecurity rulebook". Instead, the requirements are spread across a dozen Master Directions, circulars, and joint advisories — refreshed and re-issued frequently. Add to that CERT-In's parallel mandates (which apply to everyone in India, not just RBI-regulated entities) and you have a regulatory landscape that intimidates most beginners and confuses most boards.

This guide cuts through the noise. We start with who RBI actually regulates, list the cyber-security documents that matter, walk through the 24 Baseline Cyber Security Controls (BCSC) every entity needs, explain how the requirements scale up by entity type, give you a 90-day / 6-month / 12-month roadmap, and end with the audit findings RBI inspectors keep flagging in 2026. By the end you will know exactly what is required, what it costs, and what to fix first.

RBI Cybersecurity Requirements — The 60-Second Answer

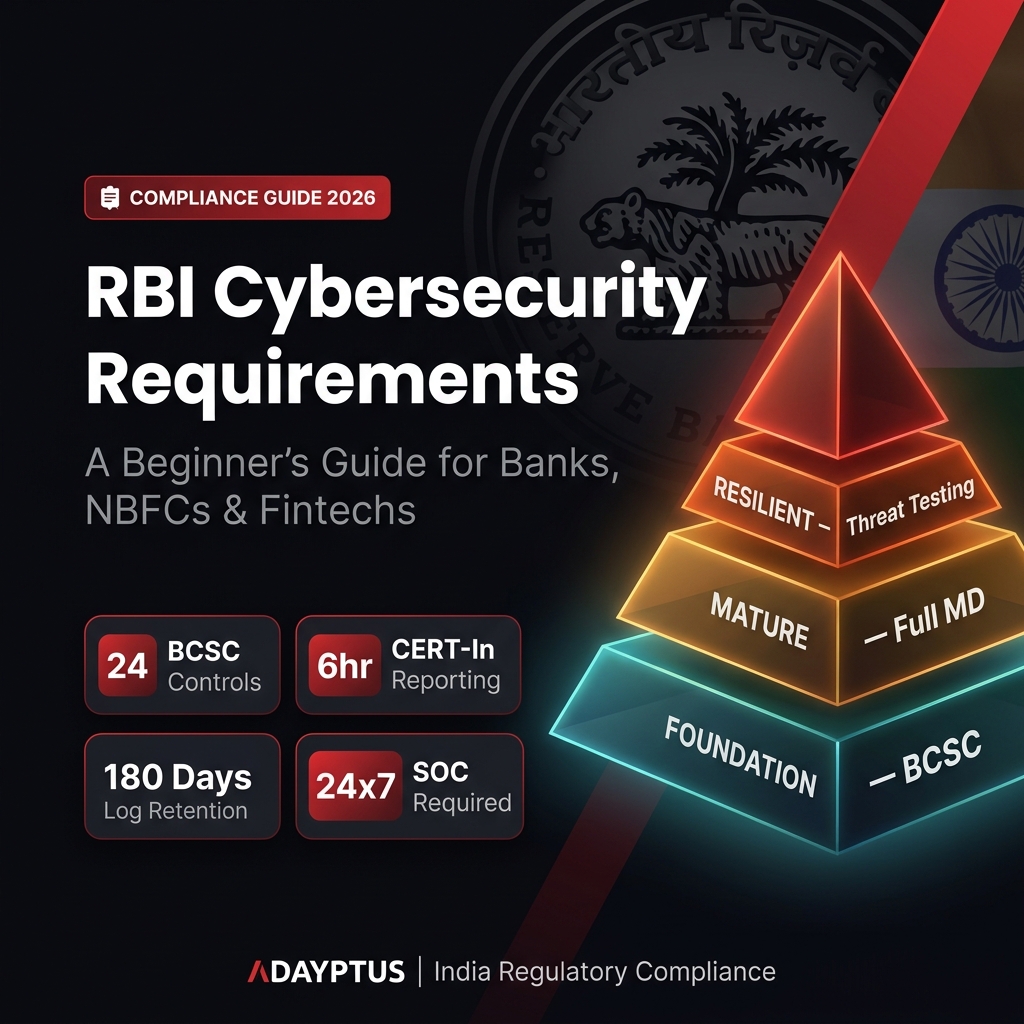

Every RBI-regulated entity — scheduled commercial bank, cooperative bank, NBFC, payment aggregator, prepaid instrument issuer, payment system operator, or non-bank PSO — is expected to operate (a) a documented cyber security policy approved by the board, (b) the 24 Baseline Cyber Security Controls (BCSC) at minimum, (c) a 24x7 Security Operations Centre or SOC partnership, (d) an annual third-party VAPT and a documented vulnerability management programme, and (e) an Information Security Audit covered under their statutory audit cycle.

Larger or systemically important entities additionally need a Cyber Crisis Management Plan (CCMP), threat-led penetration testing, IT-strategy and IT-steering committees, an independent CISO reporting to the board, and continuous compliance with the Master Direction on Information Technology Governance, Risk, Controls and Assurance Practices (2023).

In parallel, CERT-In's April 2022 Directions apply to every Indian entity and require breach reporting within 6 hours, mandatory log retention for 180 days within India, and synchronisation with NPL/NTP time servers — independent of any RBI obligation.

Who Does RBI Cyber Compliance Apply To?

RBI's cyber-security expectations are tiered by entity type. The same broad framework applies, but the depth, frequency, and audit intensity scale with size and systemic importance. Here is the practical mapping in 2026.

| Entity Type | Primary Cyber Direction | Key Asks |

|---|---|---|

| Scheduled Commercial Banks | Master Direction on Cyber Security Framework (2016, updated) | Full framework + CCMP + 24x7 CSOC + board-level CISO |

| Cooperative Banks (UCBs) | Comprehensive Cyber Security Framework for UCBs (graded approach) | Tiered controls based on bank size (Level I-IV) |

| NBFCs | Master Direction Information Technology Framework for NBFC Sector (2017+) | BCSC + IT governance + IS audit + scaled by asset size |

| Payment Aggregators / PA-PG | Master Direction on Cyber Resilience and Digital Payment Security Controls for Non-Bank PSOs (2024) | Strong cyber resilience + transaction monitoring + network segmentation |

| PPI Issuers (Wallets) | Master Direction on Digital Payment Security Controls (2021) | Customer authentication + fraud monitoring + audit trail |

| All Regulated Entities (REs) | Master Direction on IT Governance, Risk, Controls and Assurance Practices (2023) | IT strategy / steering committee, CIO + CISO, independent IS audit |

| All Indian Entities (any sector) | CERT-In Directions (April 2022) | 6-hour breach reporting + 180-day log retention + NTP sync |

The Map of RBI Cyber Documents That Matter

There is no single "RBI cybersecurity standard" — there is a stack of overlapping Master Directions, each governing a specific dimension. Beginners often get lost trying to find the one document. The truth: most regulated entities need to read and apply five-to-seven of them. Here is the working map.

1. Master Direction on Cyber Security Framework in Banks (2016, periodically updated)

The flagship document. Defines the cyber-security policy mandate, baseline controls (BCSC), Cyber Security Operations Centre (CSOC) expectations, Cyber Crisis Management Plan (CCMP), and incident reporting timelines for banks.

2. Master Direction on IT Governance, Risk, Controls and Assurance Practices (November 2023)

Applies to all regulated entities. Mandates the IT Strategy Committee, IT Steering Committee, board-approved IT and information security policies, segregation between CIO and CISO, and independent Information Systems Audit. The document most CISOs are graded against in their annual review.

3. Master Direction on Outsourcing of Information Technology Services (April 2023)

Defines how regulated entities supervise third-party IT and cloud providers. Material outsourcing arrangements require board approval, exit strategies, and vendor IS audits. The bridge between RBI cyber expectations and your hyperscaler / SaaS / managed services stack.

4. Master Direction on Digital Payment Security Controls (February 2021)

Applies to entities offering digital payment products — banks, PPI issuers, card networks. Covers customer authentication, fraud monitoring, transaction risk management, and audit trail requirements.

5. Master Direction on Cyber Resilience and Digital Payment Security Controls for Non-Bank PSOs (July 2024)

The newest in the stack. Applies to payment aggregators, PA-PG, payment gateways, and other non-bank Payment System Operators. Phased compliance through 2025-2027, with strong cyber resilience, network segmentation, and transaction-monitoring expectations.

6. Comprehensive Cyber Security Framework for Urban Cooperative Banks (UCBs)

A graded, tiered framework (Levels I-IV) that scales with the size and complexity of the cooperative bank. Smaller UCBs need Level I baseline controls; larger ones approach scheduled-commercial-bank parity.

7. CERT-In Directions (April 2022)

Not RBI, but operates in parallel. Mandates 6-hour breach reporting, 180-day log retention within Indian jurisdiction, KYC retention by VPN providers, and NTP synchronisation. Applies to all Indian entities including RBI-regulated ones.

The 24 Baseline Cyber Security Controls (BCSC) — In Plain Language

RBI's Baseline Cyber Security Controls are the 24 must-haves that show up in almost every RBI inspection. They originate in the 2016 Master Direction and have been re-emphasised in every update since. Group them by intent:

- Board-approved cyber-security policy

- Continuous IT asset inventory and classification

- Identification of critical systems / crown jewels

- Risk assessment and risk acceptance documentation

- Network segmentation, firewall, IDS/IPS

- Anti-malware on all endpoints and servers

- Patch and vulnerability management

- Secure configuration baselines (CIS / vendor)

- Application whitelisting on critical systems

- Multi-factor authentication for privileged access

- Principle of least privilege

- Quarterly user access review and recertification

- Privileged Access Management (PAM)

- Encryption at rest and in transit

- Data Leakage Prevention (DLP)

- Removable-media controls

- Secure data destruction and media sanitisation

- SIEM with correlated use cases

- 24x7 Security Operations Centre (CSOC) — own or co-managed

- EDR / endpoint behaviour monitoring

- Documented Incident Response Plan

- Cyber Crisis Management Plan (CCMP)

- Regular tabletop and incident simulation

- Backup and disaster recovery testing

- Annual VAPT and remediation tracking

An RBI inspection in 2026 typically opens by asking for evidence against this list. Have it organised, sampled, and ready before the inspector knocks.

CERT-In Directions — The Parallel Mandate

The CERT-In Directions issued under Section 70B of the IT Act, dated 28 April 2022 and effective 28 June 2022, apply alongside RBI's framework. Beginners often miss them because they sit in a different statute. The four obligations that matter:

- Six-hour breach reporting — any cybersecurity incident from a defined list (which is broad and includes ransomware, data breach, phishing, unauthorised access) must be reported to CERT-In within 6 hours of noticing or being made aware of it.

- 180-day log retention within India — ICT logs must be retained for 180 rolling days and stored in Indian jurisdiction. Cross-border log forwarding architectures require reconfiguration.

- Time synchronisation — all ICT systems must sync to NIC's NTP servers (or NPL India), to ensure consistent timestamping for forensic correlation.

- KYC and customer-data retention — VPN providers, data centres, virtual asset service providers, and intermediaries have entity-specific retention obligations.

CERT-In compliance and RBI compliance are complementary, not exclusive. Most banks satisfy both with a single SIEM, a single SOC, and a single incident-response runbook — but the runbook must explicitly call out both reporting paths (CERT-In within 6 hours, RBI within prescribed window per the Master Direction).

A 12-Month Compliance Roadmap (From a Standing Start)

If you are starting from scratch — say, a new payment aggregator post-licence, or an NBFC with limited cyber maturity — here is the realistic three-phase roadmap. Adapt the timing to your size; the sequence is what matters.

Foundation

Build the policy, governance & SOC baseline

Mature

Close gaps, deploy controls, test resilience

Resilient

Continuous validation & board-grade reporting

Realistic Cost & Timeline (2026 India Numbers)

Cost varies enormously by entity size, existing maturity, and chosen tooling. Indicative ranges for a mid-sized NBFC or a Tier-2 payment aggregator targeting full RBI cyber compliance Year 1:

₹6–15 lakh

Independent cyber-maturity gap assessment against the 24 BCSC and the relevant Master Directions.

₹40 lakh–3 cr

Co-managed or fully managed 24x7 SOC. Lower end is co-managed; upper end is fully managed enterprise SIEM + MDR.

₹15–60 lakh

Annual VAPT (web, mobile, network, cloud) plus independent IS Audit covering RBI scope.

₹30 lakh–1.5 cr

EDR, MFA, PAM, DLP, vulnerability management. Endpoint and user-count driven.

Realistic year-1 budget for a mid-sized NBFC or PA targeting full compliance: ₹1.5–5 crore depending on size, with a steady-state run-rate of ₹1–3 crore from year 2 onwards. A scheduled commercial bank or a systemically-important PSO will spend materially more on the SOC, threat intelligence, and resilience layers.

What RBI Auditors Keep Flagging in 2026

From conversations with banks, NBFCs, and PAs that have been through recent RBI inspections, the same six findings come up again and again. Treat this as a pre-inspection checklist:

Vendor / outsourcing register is incomplete High Risk

The Outsourcing Master Direction (2023) demands a documented register of all material IT outsourcing arrangements, with risk classification and exit strategies. Most entities can produce some of their cloud and SaaS contracts; few have the full register, the IS audit reports, or the documented exit plans.

Privileged access controls are weak High Risk

Shared admin accounts, no PAM session recording, no JIT elevation, infrequent privileged-access reviews. The single largest concentration of inspection findings.

Patch SLA exists on paper but not in practice Medium Risk

Policies say critical patches in 7 days, evidence shows 30+ day backlogs. Auditors sample real CVEs and ask for the patch ticket — closure dates speak for themselves.

SIEM use cases not aligned with the threat model Medium Risk

SIEM is deployed but most use cases are out-of-the-box vendor templates. No mapping to specific threat scenarios, no documented detection-engineering programme, no measurement of detection coverage.

CCMP exists but has never been exercised Medium Risk

A printed Cyber Crisis Management Plan in a binder is not evidence of resilience. Auditors ask for the dates of the last two tabletop exercises, the named participants, and the after-action minutes. Many entities cannot produce them.

CISO independence is structurally unclear Governance

The IT Governance Master Direction (2023) requires the CISO function to be independent of the CIO. Many regulated entities still have the CISO reporting into the CTO or CIO administratively. Unwind this organisationally before the inspection.

Frequently Asked Questions

Click any question to expand the answer.

Q What is the single most important RBI cybersecurity document?

For banks, the Master Direction on Cyber Security Framework in Banks (2016, periodically updated) is the foundation. For all regulated entities, the Master Direction on Information Technology Governance, Risk, Controls and Assurance Practices (November 2023) is the most-graded document because it defines organisational structure, board oversight, and audit cadence. Beginners should read both back to back.

Q Does my company need an in-house SOC, or can I outsource?

RBI does not mandate ownership of the SOC, only the outcome — 24x7 monitoring, documented detection use cases, and incident-response capability. Most mid-sized NBFCs, payment aggregators, and cooperative banks operate co-managed SOC arrangements where telemetry stays within their data sovereignty boundary while a third-party provides Tier 1 and Tier 2 analysts. See our Managed SOC vs In-House SOC guide for the build-vs-buy economics.

Q How are RBI's cybersecurity rules enforced?

Through the Information Systems Audit (IS Audit) embedded in the statutory audit cycle, periodic on-site RBI inspections, mandatory incident reporting, and post-incident enforcement. Penalties range from monetary fines and licence-restriction orders to public censure. Recent years have seen RBI publicly impose multi-crore penalties on banks and NBFCs for failures in IT governance and incident reporting.

Q What is the difference between BCSC and the full Cyber Security Framework?

The Baseline Cyber Security Controls (BCSC) are the 24 minimum controls every regulated entity is expected to operate. The full Cyber Security Framework (set out in the 2016 Master Direction) builds on BCSC with deeper expectations on the Cyber Security Operations Centre (CSOC), Cyber Crisis Management Plan (CCMP), threat-led testing, and resilience. Smaller cooperative banks operate at the BCSC tier; scheduled commercial banks operate the full framework.

Q Does ISO 27001 satisfy RBI cybersecurity requirements?

Largely, yes — at the controls layer. ISO 27001:2022's 93 Annex A controls map cleanly to most of the 24 BCSC. But ISO 27001 alone does not satisfy RBI's expectations on board oversight, IS Audit, CSOC operation, CCMP, vendor outsourcing register, or sector-specific rules like the Digital Payment Security Master Direction. Treat ISO 27001 as a strong control baseline, not a substitute. See our SOC 2 vs ISO 27001 guide for context.

Q Do I have to report every cyber incident in 6 hours?

CERT-In's 6-hour clock applies to incidents in their published list — ransomware, data breach, unauthorised access, identity theft, phishing, defacement, DoS/DDoS, and others. Routine vulnerability scans or low-impact policy violations are not in scope. Run a triage decision tree at intake so the SOC analyst knows in the first 30 minutes whether the clock has started. The RBI reporting clock is separate and triggered by the relevant Master Direction's incident definition.

Q Can I store logs and data outside India?

For RBI-regulated payment-system data, RBI's 2018 storage circular requires storage within India for end-to-end transaction data; cross-border processing is allowed but data must come back to Indian storage within 24 hours. CERT-In additionally requires 180 days of ICT logs in Indian jurisdiction. Many global SaaS and SOC providers now offer India-region data residency specifically for this reason; verify it contractually before signing.

Q How does the Digital Personal Data Protection (DPDP) Act fit with RBI rules?

DPDP and RBI cyber rules are complementary, not duplicative. DPDP governs how personal data is collected, processed, retained, and shared; RBI governs the operational cyber controls that protect it. Most mature programmes treat DPDP as the privacy programme and RBI Master Directions as the security programme, with a single mapping spreadsheet showing which controls satisfy which regulator. See our DPDP Assessment service.

How Adayptus Helps with RBI Cyber Compliance

Adayptus runs RBI cyber-compliance programmes for banks, NBFCs, payment aggregators, PPI issuers, and FinTechs across India. Our consultants speak the language of the inspector, not the language of the textbook — every output is mapped against the specific Master Direction the regulator will audit you on.

RBI Cyber Gap Assessment

Documented gap assessment against the 24 BCSC plus the relevant entity-specific Master Direction. Output: a board-ready remediation roadmap with named owners, SLAs, and budget.

Co-Managed SOC for RBI Entities

24x7 SOC operating on your SIEM in India-region cloud. Detection use cases mapped to the Master Direction. Audit-ready evidence library generated automatically.

Annual VAPT & IS Audit

Independent third-party VAPT covering web, mobile, network, cloud, and API surfaces. Reports formatted to match RBI inspection expectations.

Threat-Led Testing

Adversary emulation aligned to RBI's threat-led penetration testing expectations. Sector-relevant actor profiling for BFSI.

Virtual CISO & Board Reporting

Independent CISO function structurally separate from the CIO, exactly as the IT Governance Master Direction expects. Board-ready quarterly cyber dashboards.

Cyber Crisis Tabletops

CCMP-aligned tabletop exercises and ransomware response simulations. Documented after-action reports the inspector will actually accept.

Walk into your next RBI inspection with the evidence ready.

A 60-minute scoping call with our regulatory practice. We will tell you which Master Directions apply to your entity, where your highest-risk gaps are right now, and how a 12-month remediation programme would actually unfold — in inspector-grade detail.

Conclusion: Build the Foundation, Then Mature

RBI cybersecurity compliance is not a single document or a one-off audit; it is an operating discipline that, once built, runs alongside your business indefinitely. Beginners often try to do everything at once and burn out at month four. The discipline that wins is sequencing: foundation first (board policy, asset inventory, BCSC, SOC), maturity second (full Master Direction implementation, IS audit, vendor governance), resilience third (threat-led testing, continuous validation, board-grade reporting).

If you are reading this because an RBI inspection is on the horizon and you are not sure whether you will pass — start with the gap assessment this week. Most of the findings inspectors flag are not exotic; they are foundational, fixable in 90 days, and deferred only because nobody owns the work. Pick the owner, run the gap, build the roadmap, ship the controls, and the next inspection becomes a routine event instead of a board-level crisis. Our regulatory compliance team does this every week — happy to help.

Peyush Baranwal

Senior Delivery Manager — Cyber Security, Adayptus

Peyush Baranwal is a Senior Delivery Manager at Adayptus Consulting with 11+ years of experience designing, implementing, and managing enterprise security programmes. His core expertise spans Vulnerability Assessment & Penetration Testing (VAPT), Application Security, and Security Operations — leading web, mobile, API, and infrastructure security assessments for CISOs and security teams across BFSI, healthcare, and SaaS. He focuses on measurable risk reduction, governance maturity, and operationalising detection-and-response capability. Outside work, Peyush is a passionate biker and part-time photographer.

Connect on LinkedInExecutive Intelligence Briefing

Join top security executives receiving our curated analysis of zero-days, compliance shifts, and architectural vulnerabilities—delivered completely ad-free.

On This Page

- RBI Cybersecurity Requirements — The 60-Second Answer

- Who Does RBI Cyber Compliance Apply To?

- The Map of RBI Cyber Documents That Matter

- The 24 Baseline Cyber Security Controls (BCSC) — In Plain Language

- CERT-In Directions — The Parallel Mandate

- A 12-Month Compliance Roadmap (From a Standing Start)

- Realistic Cost & Timeline (2026 India Numbers)

- What RBI Auditors Keep Flagging in 2026

- Frequently Asked Questions

- How Adayptus Helps with RBI Cyber Compliance

- Conclusion: Build the Foundation, Then Mature